It seems like we just can’t stop talking about central banks. And this week will be no different, with at least 15 central bank meetings planned, some more important than others, of course. While the Federal Reserve (Fed) meeting will likely take top billing in the financial media, it’s the Bank of Japan (BOJ) meeting on Tuesday that could be the real game changer. With inflationary pressures still above target in Japan, the BOJ may finally be ready to take interest rates out of negative territory for the first time since 2016. If true, the era of free money will finally be over, which could have an impact on U.S. markets.

Central bankers from the U.S. to Australia and seemingly everywhere in between will be meeting this week to discuss monetary policy. A total of 15 meetings will take place this week, highlighted by the Fed, the Bank of England (BOE) and the BOJ. After years of central banks tightening monetary policy by raising interest rates, markets (and consumers) are waiting for interest rates to come back down. Unfortunately, despite falling inflationary pressures, it may be a few more months until central bankers are ready to start lowering interest rates. That doesn’t mean these meetings won’t be worth watching; we think they will be, especially the Fed and BOJ meetings.

Just a Little Patience

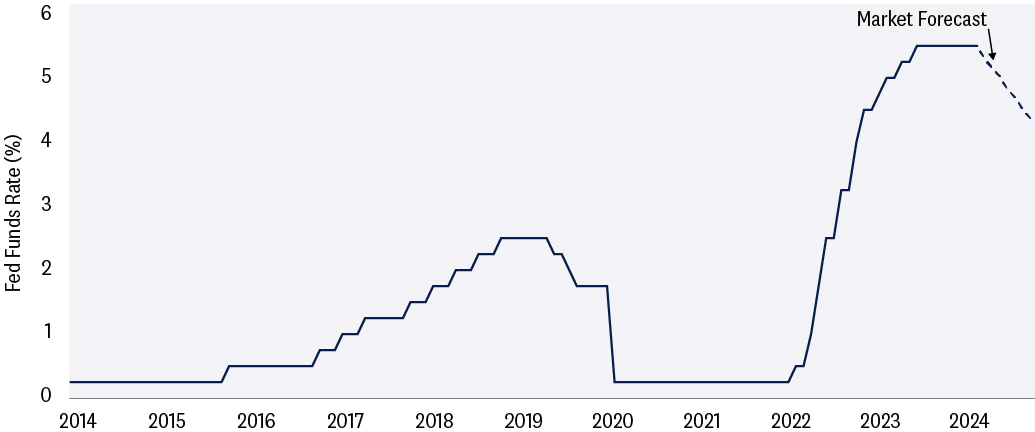

On Wednesday, the Fed will conclude its two-day meeting where it is unlikely it will change short-term interest rates. At 5.3% (effective rate), the fed funds rate has remained unchanged since its July 2023 meeting, and it looks like it will be a few more meetings until the Fed is comfortable enough with existing progress on inflation to start to lower interest rates. The Fed has preached patience recently, acknowledging progress, but they want more evidence that inflation is headed back to its 2% target. Markets, of course, are forward-looking and have currently priced in around three cuts this year, which would take the fed funds rate close to 4.5%.

Markets Expect the Fed to Cut Rates Three Times This Year

And a Fed Funds Rate Down to 4.5% by Year-end

Source: LPL Research, Bloomberg, 03/13/24

Past performance is no guarantee of future results.

Economic forecasts set forth may not develop as predicted and are subject to change.

Along with the interest rate decision, the Fed updates its Summary of Economic Projections (SEP) four times a year, which is the Fed’s expectations on inflation and economic growth. With general softening of economic data (although still resilient), but perhaps stickier inflation than expected, markets will certainly be paying attention to the Fed’s forecast on economic growth, inflation, and unemployment.

Beware of the Dots

Along with the SEP, the Fed releases its “dot plot”, which represents the expected path of short-term interest rates by Fed members. Each dot represents a member’s opinion on where the Fed funds policy rate should be over the next few years. While not official policy, it does provide additional transparency into Fed member thinking — albeit anonymously.

In December, which was the last time the dot plot was released, the Fed, in aggregate, expected three rate cuts in 2024; however, the opinions of individual members ranged from no cuts to six cuts. So, while the “median” member expected three cuts, it would only take two members (out of 17) to change their view to reflect only two expected cuts in 2024.

Our view:The stickiness of services inflation will likely push out the first rate cut. We’ve always thought the markets were overly zealous in thinking the Fed would cut six or seven times this year. The Fed communicated three cuts, and we expect three or four rate cuts this year as well. However, historically, the Fed hardly ever does what it says, as evidence that dot plots are poor predictors of future Fed policy is clear.

The first rate cut will now probably come in June, unless something drastic happens domestically or abroad. Labor markets are stable, consumers keep spending, and geopolitical tensions are managed enough for the Fed to have lingering concerns about price stability.

After the Fed’s embarrassing mistake of keeping rates too low for too long and capital markets still reeling from the effects of that mistake, the Fed will not be inclined to make a similar misstep of cutting rates too soon.

The Times They Are A-Changin’

Aside from the Fed meeting, markets will be watching for a potential change in monetary policy out of the BOJ. For over a decade, the BOJ has emphasized that a “virtuous cycle of wages and prices” is essential for the stable and sustainable achievement of its 2% inflation target. Japan, for several decades, has been stuck largely in a low growth, low inflation regime. However, consumer prices grew by 3.3% in 2023 and are expected to grow by 2.2% in 2024. Both inflation and wages are on the verge of a change, escaping from a low inflation/wage growth equilibrium.

Japan’s largest union group announced stronger-than-expected annual wage increases last Friday. Rengo, a federation of unions, said its members have so far secured deals averaging 5.3%, a figure that far outpaces the initial 3.8% tally from a year ago — itself the biggest in 30 years. Many of Rengo’s affiliated groups had already announced agreements to hike wages by 5% or more. The challenge for Japan over recent decades has been a lack of consumption stemming from low wage growth. BOJ officials, including BOJ Governor Kazuo Ueda, have recently stressed the timing of a shift away from negative rates would depend on the outcome of this year's annual wage negotiations between workers and employers. Thus, improved wage negotiations likely provide the BOJ with more confidence to finally take interest rates out of negative territory.

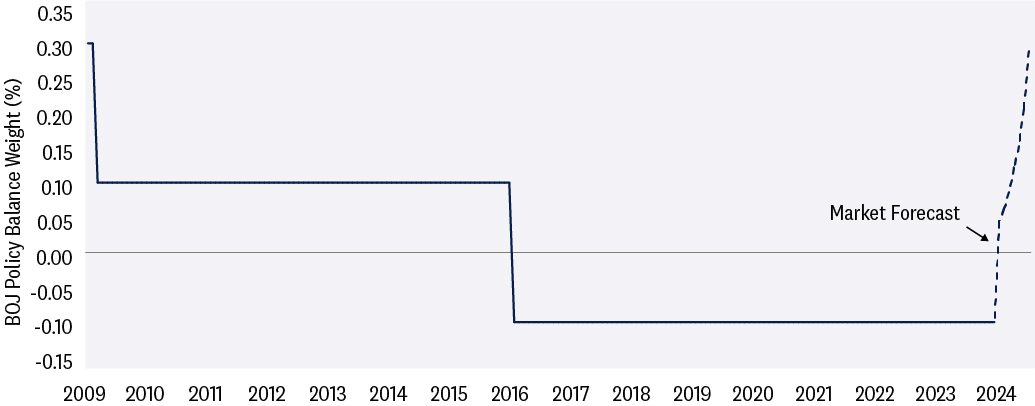

Since 2016, the main policy rate for the BOJ has been stuck at -0.10%. But with improved wage negotiations, markets are expecting a 0.10% rate hike this week from the BOJ, the first hike since 2007. Additionally, markets expect the main policy rate to climb to 0.25% by year-end.

Historic Interest Rate Shift Coming?

Markets Expect the Bank of Japan to Finally Raise Interest Rates

Source: LPL Research, Bloomberg, 03/13/24

Past performance is no guarantee of future results.

Economic forecasts set forth may not develop as predicted and are subject to change.

Moreover, upon exiting its negative rate policy, according to Reuters, the BOJ will also ditch its bond yield curve control and discontinue purchases of risky assets such as exchange-traded funds (ETF), putting a formal end to the most aggressive monetary accommodation of former Governor Haruhiko Kuroda, which has been in place since 2013. To borrow a phrase from Bob Dylan, the times, they are a-changin’.

Expected Impact on U.S. Fixed Income Markets

With Fed rate cuts still on hold and a potential exit from negative interest rates in Japan, investors may be concerned about the impact these decisions will have on U.S. fixed income markets. Treasury markets have recently become more better aligned with the Fed’s view on rate cuts, so a reduction in cuts on the dot plot may push bond yields higher. However, we think it’s a matter of when rate cuts happen, not if. We still expect rate cuts this year, but in the meantime, it has meant higher bond yields/lower bond prices and higher interest rate volatility. And once rate cuts do come, we’re likely going to see lower interest rates (higher prices) along the U.S. Treasury yield curve.

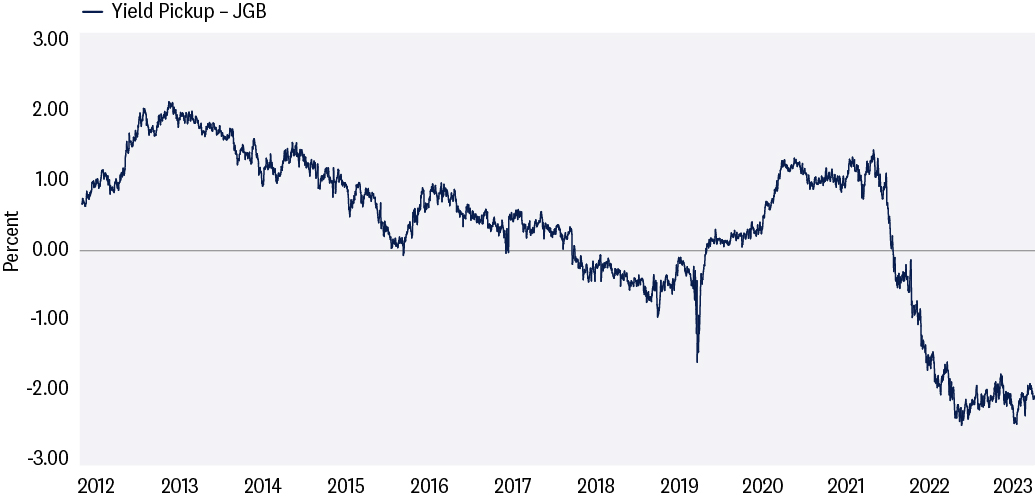

Regarding policy normalization from the BOJ (read higher domestic interest rates), the risk is that Japanese investors shun U.S. markets for domestic markets. Japan is the largest non-domestic owner of U.S. Treasuries, so a scenario in which Japanese investors repatriate their capital back to domestic markets would likely negatively influence U.S. Treasury yields and push yields higher. However, we think that risk is still fairly low. First, policy normalization is expected to be slow and only incremental. A 0.25% increase to policy rates and perhaps a 1% yield on the 10-year Japanese government bond (JGB) yield is unlikely enough for Japanese investors to rush out of U.S. investments. Moreover, over the last few years, despite being one of the largest owners of U.S. Treasuries, Japanese investors haven’t been big buyers of Treasuries. It just simply hasn’t been a very attractive trade recently.

When investing in U.S. markets, foreign investors must be mindful of the currency risk associated with U.S. investments. Because foreign investors’ liabilities are denominated in their home currency (in this case Japanese yen), most foreign investors hedge out the dollar risk embedded within U.S. investments. There is a cost to hedging out that risk though, which limits the attractiveness of those cross-border investments. And since 2022, on a currency-adjusted basis, despite very low interest rates in Japan, Japanese investors were better served by investing locally and not buying U.S. assets. So, as long as the dollar remains strong relative to the yen, it is unlikely Japanese investors will be big buyers of U.S. Treasuries regardless of expected policy normalization from the BOJ.

10-year Treasury Yields Are Not Attractive to Japanese Investors

Difference in 10-year Foreign Treasury Yield vs. 10-Year U.S. Treasury Yield Hedged to Foreign Currency

Source: LPL Research, Bloomberg, 03/13/24

All indexes are unmanaged and cannot be invested into directly.

Past performance is no guarantee of future results.

Conclusion

Central banks have been one of the biggest stories in global capital markets over the last few years, and it looks like they will be for a few more quarters. This week will be a busy one for central banks, but aside from the BOJ, we think the next move for bankers is to lower interest rates and not raise them. We think the Fed is on hold until the summer months but in general, we expect lower policy rates by the end of this year. This rings true, in our opinion, for the BOE and the European Central Bank (one of the few not meeting this week) as well. And with the BOJ starting to normalize policy rates as well, it’s likely we’re getting back to a more normal interest rate environment, which is ultimately a good thing for markets.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its neutral equities stance despite the strength of the latest stock market rally that has carried the S&P 500 over the 5,000 milestone. The improved outlook for economic growth and earnings, along with relative stability in interest rates, keeps the risk-reward trade-off for stocks and bonds fairly well balanced still, though upside over the rest of the year is likely to be modest.

Within equities, the STAAC continues to favor a tilt toward domestic over international equities, with a preference for Japan among developed markets, and an underweight position in emerging markets (EM). The Committee also recommends slight tilts toward large caps and growth stocks. Finally, the STAAC continues to recommend a modest overweight to fixed income, funded from cash.

Jeffrey Roach,PhD, Chief Economist

Lawrence Gillum,CFA, Chief Fixed Income Strategist

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time.

The prices of small cap stocks are generally more volatile than large cap stocks.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

LPL Financial does not provide investment banking services and does not engage in initial public offerings or merger and acquisition activities.

Precious metal investing involves greater fluctuation and potential for losses.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered inv estment advisor and broker -dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment a dvice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

| Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value |

RES-000823-0224 | For Public Use | Tracking #553977 (Exp. 03/2025)